In the world of finance, there are various financial instruments that professionals use to manage risk and hedge against future uncertainties. One such instrument is a Forward Rate Agreement (FRA). In this article, we will explore what a FRA is, how it works, and its significance in the financial markets.

A Forward Rate Agreement is a contract between two parties to exchange a fixed interest rate for a floating interest rate at a predetermined future date. It is essentially an agreement to lock in a borrowing or lending rate for a specific period in the future. FRAs are commonly used by banks, corporations, and investors to hedge against interest rate fluctuations or to speculate on future interest rate movements.

The mechanics of a FRA are relatively straightforward. Let's say a bank expects interest rates to rise in the future and wants to protect itself against this risk. The bank can enter into a FRA with another party, such as another bank or an investor. The FRA would specify the notional amount, the reference interest rate (usually LIBOR), the fixed interest rate, and the maturity date.

At the maturity date, if the reference interest rate is higher than the fixed interest rate specified in the FRA, the party that sold the FRA (the party receiving the fixed rate) would pay the difference to the party that bought the FRA (the party receiving the floating rate). Conversely, if the reference interest rate is lower than the fixed interest rate, the party that bought the FRA would pay the difference to the party that sold the FRA.

The key benefit of using FRAs is that they allow parties to hedge against interest rate risk without actually entering into a loan or investment. This means that parties can protect themselves against potential losses or gains without having to commit additional capital.

FRAs also provide flexibility in managing interest rate risk. For example, if a bank has already entered into a loan agreement with a fixed interest rate but wants to convert it into a floating rate, it can enter into an offsetting FRA to effectively convert the fixed rate into a floating rate. This allows the bank to align its liabilities with its assets and better manage its overall risk exposure.

Furthermore, FRAs are traded in the over-the-counter (OTC) market, which means they are customizable and can be tailored to specific needs. Parties can negotiate the terms of the FRA, such as the notional amount, maturity date, and fixed interest rate. This flexibility allows market participants to design FRAs that best suit their risk management strategies.

It is worth noting that while FRAs are commonly used for hedging purposes, they can also be used for speculative purposes. Speculators may enter into FRAs to profit from anticipated changes in interest rates. However, it is important to remember that speculation carries its own risks and should only be undertaken by those with a thorough understanding of the market dynamics.

In conclusion, a Forward Rate Agreement is a financial instrument that allows parties to hedge against interest rate risk or speculate on future interest rate movements. It provides flexibility, customization, and capital efficiency in managing risk exposure. However, like any financial instrument, it should be used judiciously and with a clear understanding of its implications. As with any investment or hedging strategy, it is advisable to seek professional advice before entering into any FRA transactions.

Related News

What is a time deposit and how does it work

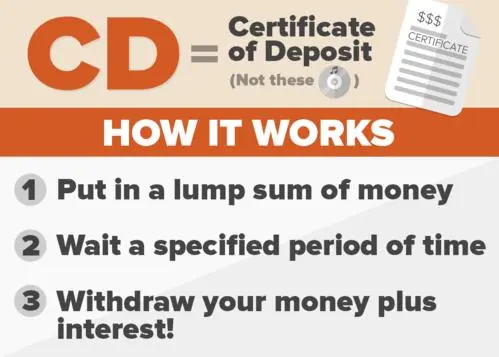

A time deposit, commonly known as a certificate of deposit (CD), is a type of savings account offered by banks and financial institutions. It operates as a fixed-term deposit where you agree to keep a specific amount of money deposited for a predetermined period, known as the term or maturity period BANKING2026-07-20

Fintech: The Key to Financial Inclusion in Nigeria

TranscriptBank of Industry is Nigeria’s oldest, largest, and most successful development finance institution. Over the last six years it has provided financing to over four million enterprises, helpin... BANKING2026-06-19

How Akwa Ibom Became an FDI Magnet by Transforming from a Civil Service State

TranscriptUdom Emmanuel took governorship of the Nigerian state Akwa Ibom in 2015. Since then he has transformed the southern coastal region from a civil service state into an attractive destination f... BANKING2026-07-15

There are several ways to deposit money in a bank

There are various ways to deposit money in a bank, and the availability of these methods can depend on the specific bank and its services. Here are some common ways to deposit money into a bank:1. Cash Deposit at the Branch:- You can visit the physical branch of the bank and BANKING2026-06-20

Advancing Financial Inclusion in Nigeria: A Journey of Transformation

Lagos, NigeriaBanking|Commercial bankingAuthor:Urum Kalu Eke, Group Managing Director, FBN HoldingsTop 5Top 5 forces that will shape international finance in 2023Top 5 female-fronted fintech firmsTop ... BANKING2026-07-18

Navigating Sanctions: European Countries Establish Trade Mechanism with Iran

Tehran, Iran. The country's oil industry has been particularly baldy hit by the recent US sanctions and this new European mechanism will not cover transactions related to this sectorFeatured|MarketsAu... BANKING2026-07-22

How can I earn the highest interest on my money in the bank

Earning the highest interest on your money in a bank often involves considering different types of bank accounts and financial instruments. Here are some strategies to potentially maximize the interest you earn:1. High-Yield Savings Account:- Consider opening a high-yield savings account BANKING2026-07-05