Money and credit are two essential concepts in banking, as they determine how banks operate and how they affect the economy. Money is any item that is generally accepted as a medium of exchange, a unit of account, and a store of value. Credit is the ability to obtain goods or services before payment, based on the trust that payment will be made in the future. Banks are involved in both the creation and the management of money and credit, as they perform two main functions: intermediation and regulation1.

Intermediation

Intermediation is the process of connecting savers and borrowers, or lenders and investors, through financial intermediaries such as banks. Banks accept deposits from customers who have surplus money and lend them to customers who need money. Banks make use of deposits to meet the loan requirements of the people. Thus, in this way, the banks mediate between those who have surplus money and those who need money2. Banks charge a higher interest rate on loans than what they offer on deposits. The difference between the two is the main source of income of the banks2.

By lending out the deposits they receive, banks create money in the form of bank credit. Bank credit is the amount of credit available to a business or individual from a banking institution in the form of loans3. Bank credit is also known as bank money, as it can be used as a medium of exchange by the borrowers. Bank money is a type of fiat money, which means it is not backed by any physical commodity, but by the trust and confidence of the public. Bank money is a significant component of the money supply, which is the total amount of money available in an economy3.

Banks also provide other types of credit, such as credit cards, mortgages, car loans, and business lines of credit. These are different ways of borrowing money for various purposes and durations. Credit cards allow customers to buy goods and services on credit and pay them back later, usually with interest. Mortgages are loans secured by real estate property, such as houses or apartments. Car loans are loans secured by vehicles, such as cars or trucks. Business lines of credit are flexible loans that allow businesses to access funds as needed, up to a certain limit3.

Regulation

Regulation is the process of controlling and supervising the banking system by the authorities, such as central banks and government agencies. Regulation aims to ensure the stability and efficiency of the banking system, as well as to protect the interests of the customers and the public. Regulation involves setting rules and standards for banks to follow, such as capital requirements, reserve ratios, liquidity ratios, and prudential norms. Regulation also involves monitoring and enforcing compliance with these rules and standards, as well as intervening in case of problems or crises1.

Central banks are the authorities that manage the monetary system for a country or a group of countries. They are responsible for issuing currency, setting interest rates, regulating banks, and implementing monetary policy to achieve macroeconomic goals such as price stability, full employment, and economic growth. Central banks also act as lenders of last resort, providing emergency funds to banks and other financial institutions in times of crisis1. Examples of central banks are the Federal Reserve in the U.S., the European Central Bank in the eurozone, and the Bank of Japan in Japan1.

Government agencies are the authorities that oversee the banking sector and protect the rights and interests of the customers and the public. They are responsible for licensing and supervising banks, ensuring consumer protection, promoting financial inclusion, and resolving disputes and complaints. Government agencies also act as deposit insurance providers, guaranteeing the safety of the deposits in case of bank failures. Examples of government agencies are the Federal Deposit Insurance Corporation (FDIC) in the U.S., the Financial Services Agency (FSA) in Japan, and the Prudential Regulation Authority (PRA) in the U.K.1.

Conclusion

Money and credit are two interrelated concepts that define how banks operate and how they affect the economy. Banks create and manage money and credit through intermediation and regulation, providing various services to customers and contributing to economic growth and stability. By understanding the roles and functions of banks, as well as the types and sources of money and credit, you can make better financial decisions and optimize your banking experience.

Related News

What is a time deposit and how does it work

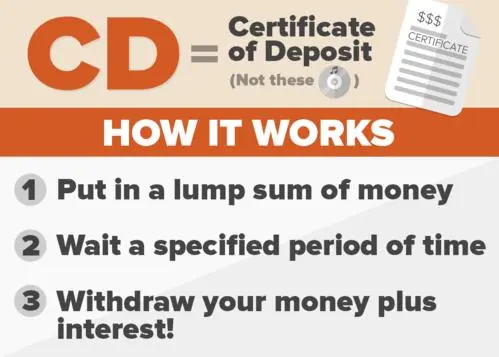

A time deposit, commonly known as a certificate of deposit (CD), is a type of savings account offered by banks and financial institutions. It operates as a fixed-term deposit where you agree to keep a specific amount of money deposited for a predetermined period, known as the term or maturity period BANKING2026-07-20

Fintech: The Key to Financial Inclusion in Nigeria

TranscriptBank of Industry is Nigeria’s oldest, largest, and most successful development finance institution. Over the last six years it has provided financing to over four million enterprises, helpin... BANKING2026-06-19

How Akwa Ibom Became an FDI Magnet by Transforming from a Civil Service State

TranscriptUdom Emmanuel took governorship of the Nigerian state Akwa Ibom in 2015. Since then he has transformed the southern coastal region from a civil service state into an attractive destination f... BANKING2026-07-15

There are several ways to deposit money in a bank

There are various ways to deposit money in a bank, and the availability of these methods can depend on the specific bank and its services. Here are some common ways to deposit money into a bank:1. Cash Deposit at the Branch:- You can visit the physical branch of the bank and BANKING2026-06-20

Advancing Financial Inclusion in Nigeria: A Journey of Transformation

Lagos, NigeriaBanking|Commercial bankingAuthor:Urum Kalu Eke, Group Managing Director, FBN HoldingsTop 5Top 5 forces that will shape international finance in 2023Top 5 female-fronted fintech firmsTop ... BANKING2026-07-18

Navigating Sanctions: European Countries Establish Trade Mechanism with Iran

Tehran, Iran. The country's oil industry has been particularly baldy hit by the recent US sanctions and this new European mechanism will not cover transactions related to this sectorFeatured|MarketsAu... BANKING2026-07-22

Udom Emmanuel’s Vision: Bringing Private Sector Discipline to Public Sector

TranscriptUdom Emmanuel took governorship of the Nigerian state Akwa Ibom in 2015. Since then he has transformed the southern coastal region from a civil service state into an attractive destination f... BANKING2026-07-11

How can I earn the highest interest on my money in the bank

Earning the highest interest on your money in a bank often involves considering different types of bank accounts and financial instruments. Here are some strategies to potentially maximize the interest you earn:1. High-Yield Savings Account:- Consider opening a high-yield savings account BANKING2026-07-05