Banks are financial institutions that provide various services to individuals, businesses, and governments. They are essential for the functioning of the economy, as they facilitate the flow of money, credit, and investments. However, not all banks are the same. There are different types of banks that specialize in different areas and serve different customers. In this article, we will explore the main categories of banks and their differences.

Central Banks

Central banks are the authorities that manage the monetary system for a country or a group of countries. They are responsible for issuing currency, setting interest rates, regulating banks, and implementing monetary policy to achieve macroeconomic goals such as price stability, full employment, and economic growth. Central banks also act as lenders of last resort, providing emergency funds to banks and other financial institutions in times of crisis. Examples of central banks are the Federal Reserve in the U.S., the European Central Bank in the eurozone, and the Bank of Japan in Japan

Retail and Commercial Banks

Retail and commercial banks are the most common types of banks that deal with the general public and businesses. They offer basic banking services such as checking and savings accounts, loans, credit cards, and foreign exchange. Retail banks focus on consumers and small businesses, while commercial banks cater to larger corporations and institutions. Retail and commercial banks operate through physical branches, ATMs, online platforms, and mobile apps. They make money by charging fees for their services and by earning interest from lending out the deposits they receive from their customers

Investment Banks

Investment banks help businesses and governments raise capital in the financial markets. They do this by underwriting securities, such as stocks and bonds, and selling them to investors. They also provide advisory services, such as mergers and acquisitions, restructuring, and valuation. Investment banks often work with corporate clients, but they may also deal with high-net-worth individuals and institutional investors, such as pension funds and hedge funds. Investment banks are usually separate from retail and commercial banks, but some banks may have both divisions. Examples of investment banks are Goldman Sachs, Morgan Stanley, and JPMorgan Chase

Private Banks

Private banks provide exclusive services to wealthy clients, usually those with at least $1 million of net worth. They help clients manage their wealth, provide tax advice, and set up trusts to avoid taxes when leaving money to descendants. Private banks also offer customized investment solutions, such as private equity, hedge funds, and real estate. Private banks are different from retail and commercial banks, as they offer more personalized and confidential services. They also charge higher fees and require higher minimum balances. Examples of private banks are UBS, Credit Suisse, and HSBC

Other Types of Banks

Besides the four main categories of banks, there are also other types of banks that serve specific purposes or niches. Some examples are:

Credit unions: These are not-for-profit organizations that are owned by their members, who share some characteristics in common, such as where they live, their occupation, or an organization they belong to. Credit unions offer similar products and services as retail banks, but they usually charge lower fees and pay higher interest rates. They are also regulated differently and have more limited access to the financial markets.

Savings and loan associations: These are financial institutions that specialize in accepting savings deposits and making mortgage loans. They are also known as thrifts or mutual savings banks. They are similar to retail banks, but they focus more on residential lending and community development. They are also regulated differently and have more limited access to the financial markets.

Online banks: These are banks that operate entirely online, without any physical branches or ATMs. They offer similar products and services as retail banks, but they usually charge lower fees and pay higher interest rates. They also have more convenience and flexibility, as customers can access their accounts anytime and anywhere. However, they may also have less security and customer service, as well as limited cash access.

Conclusion

Banks are diverse and complex institutions that play a vital role in the economy. They provide various services to different customers, depending on their needs and preferences. By understanding the different types of banks and their differences, you can choose the best bank for you and make the most of your banking experience.

Related News

What is a time deposit and how does it work

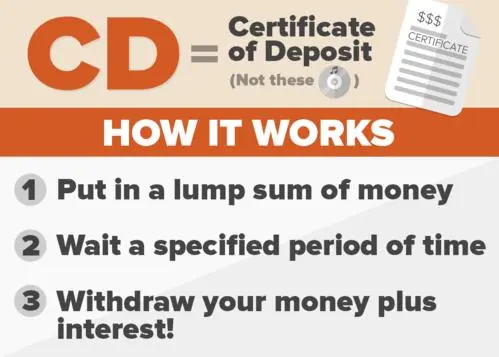

A time deposit, commonly known as a certificate of deposit (CD), is a type of savings account offered by banks and financial institutions. It operates as a fixed-term deposit where you agree to keep a specific amount of money deposited for a predetermined period, known as the term or maturity period BANKING2026-07-20

Fintech: The Key to Financial Inclusion in Nigeria

TranscriptBank of Industry is Nigeria’s oldest, largest, and most successful development finance institution. Over the last six years it has provided financing to over four million enterprises, helpin... BANKING2026-08-03

How Akwa Ibom Became an FDI Magnet by Transforming from a Civil Service State

TranscriptUdom Emmanuel took governorship of the Nigerian state Akwa Ibom in 2015. Since then he has transformed the southern coastal region from a civil service state into an attractive destination f... BANKING2026-07-15

There are several ways to deposit money in a bank

There are various ways to deposit money in a bank, and the availability of these methods can depend on the specific bank and its services. Here are some common ways to deposit money into a bank:1. Cash Deposit at the Branch:- You can visit the physical branch of the bank and BANKING2026-08-01

Advancing Financial Inclusion in Nigeria: A Journey of Transformation

Lagos, NigeriaBanking|Commercial bankingAuthor:Urum Kalu Eke, Group Managing Director, FBN HoldingsTop 5Top 5 forces that will shape international finance in 2023Top 5 female-fronted fintech firmsTop ... BANKING2026-07-18

Navigating Sanctions: European Countries Establish Trade Mechanism with Iran

Tehran, Iran. The country's oil industry has been particularly baldy hit by the recent US sanctions and this new European mechanism will not cover transactions related to this sectorFeatured|MarketsAu... BANKING2026-07-22

Udom Emmanuel’s Vision: Bringing Private Sector Discipline to Public Sector

TranscriptUdom Emmanuel took governorship of the Nigerian state Akwa Ibom in 2015. Since then he has transformed the southern coastal region from a civil service state into an attractive destination f... BANKING2026-07-11

How can I earn the highest interest on my money in the bank

Earning the highest interest on your money in a bank often involves considering different types of bank accounts and financial instruments. Here are some strategies to potentially maximize the interest you earn:1. High-Yield Savings Account:- Consider opening a high-yield savings account BANKING2026-07-05