In the world of finance, the failure of a bank is not an uncommon occurrence. While it may seem perplexing that a bank can go under and yet borrowers are still expected to repay their loans, there are several factors at play that explain this seemingly paradoxical situation.

First and foremost, it is important to understand that a bank's failure does not absolve borrowers of their contractual obligations. When you take out a loan from a bank, you enter into a legally binding agreement to repay the borrowed funds, regardless of the bank's financial health. This agreement remains valid even if the bank fails, as the loan contract is a separate entity from the bank itself.

Secondly, when a bank fails, it typically undergoes a process called liquidation. This involves the sale of the bank's assets to repay its debts and obligations. Loans are considered assets of the bank, and they are included in this liquidation process. In most cases, loans are transferred to another financial institution or a government agency, which then assumes responsibility for collecting repayments from borrowers.

It is worth noting that during a bank failure, there may be a period of uncertainty and disruption in the loan servicing process. Borrowers might experience delays or changes in how they make their loan payments. However, it is important to remember that the obligation to repay the loan remains in effect, even if there are temporary disruptions or changes in the loan servicing arrangements.

Furthermore, in some cases, government intervention may occur to prevent widespread financial instability. Governments may step in to provide financial support or facilitate the acquisition of a failing bank by a stronger institution. These measures aim to protect depositors and borrowers, ensuring that the financial system continues to function smoothly.

From a borrower's perspective, it can be frustrating to be caught in the middle of a bank failure. However, it is crucial to maintain open lines of communication with the institution handling your loan and stay informed about any changes or updates regarding your repayment obligations. Ignoring or neglecting your loan repayment responsibilities can have serious consequences for your creditworthiness and financial future.

In conclusion, while it may seem counterintuitive, the failure of a bank does not absolve borrowers of their loan repayment obligations. Loan contracts remain valid even if the bank fails, and borrowers are still expected to fulfill their contractual commitments. Understanding these dynamics and staying informed about any changes or disruptions in the loan servicing process is essential for navigating through such challenging situations.

Related News

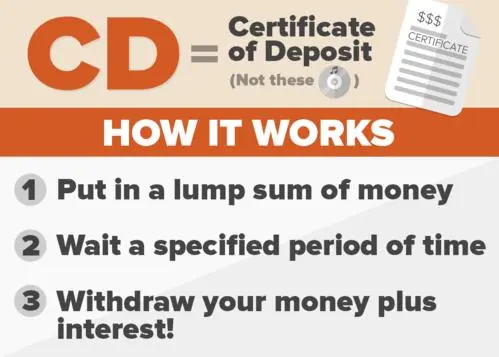

What is a time deposit and how does it work

A time deposit, commonly known as a certificate of deposit (CD), is a type of savings account offered by banks and financial institutions. It operates as a fixed-term deposit where you agree to keep a specific amount of money deposited for a predetermined period, known as the term or maturity period BANKING2026-07-20

Fintech: The Key to Financial Inclusion in Nigeria

TranscriptBank of Industry is Nigeria’s oldest, largest, and most successful development finance institution. Over the last six years it has provided financing to over four million enterprises, helpin... BANKING2026-08-03

How Akwa Ibom Became an FDI Magnet by Transforming from a Civil Service State

TranscriptUdom Emmanuel took governorship of the Nigerian state Akwa Ibom in 2015. Since then he has transformed the southern coastal region from a civil service state into an attractive destination f... BANKING2026-07-15

There are several ways to deposit money in a bank

There are various ways to deposit money in a bank, and the availability of these methods can depend on the specific bank and its services. Here are some common ways to deposit money into a bank:1. Cash Deposit at the Branch:- You can visit the physical branch of the bank and BANKING2026-08-01

Advancing Financial Inclusion in Nigeria: A Journey of Transformation

Lagos, NigeriaBanking|Commercial bankingAuthor:Urum Kalu Eke, Group Managing Director, FBN HoldingsTop 5Top 5 forces that will shape international finance in 2023Top 5 female-fronted fintech firmsTop ... BANKING2026-07-18

Navigating Sanctions: European Countries Establish Trade Mechanism with Iran

Tehran, Iran. The country's oil industry has been particularly baldy hit by the recent US sanctions and this new European mechanism will not cover transactions related to this sectorFeatured|MarketsAu... BANKING2026-07-22

Udom Emmanuel’s Vision: Bringing Private Sector Discipline to Public Sector

TranscriptUdom Emmanuel took governorship of the Nigerian state Akwa Ibom in 2015. Since then he has transformed the southern coastal region from a civil service state into an attractive destination f... BANKING2026-07-11

How can I earn the highest interest on my money in the bank

Earning the highest interest on your money in a bank often involves considering different types of bank accounts and financial instruments. Here are some strategies to potentially maximize the interest you earn:1. High-Yield Savings Account:- Consider opening a high-yield savings account BANKING2026-07-05