The recent collapse of Silicon Valley Bank and Signature Bank has raised concerns about the safety of bank deposits and the role of the Federal Deposit Insurance Corporation (FDIC) in protecting them. The FDIC is a government agency that insures deposits in most U.S. banks and thrifts up to $250,000 per depositor, per bank, per account type. The FDIC also has the authority to invoke a “systemic risk” exception and guarantee all deposits, both insured and uninsured, in a failed bank that poses a threat to the stability of the financial system. This is what happened with Silicon Valley Bank and Signature Bank, which were deemed “systemically important” by federal regulators.

But what does this mean for the average depositor? How likely is it that your bank will fail and you will get your money back? And what are the costs and benefits of deposit insurance?

The likelihood of bank failure

Bank failures are rare events, but they do happen. According to the FDIC, there have been 563 bank failures since 2000, with the peak occurring in 2010, when 157 banks failed. The most common causes of bank failure are bad loans, fraud, mismanagement, or external shocks, such as recessions, natural disasters, or pandemics. When a bank fails, the FDIC steps in as the receiver and tries to sell its assets and liabilities to another bank or operate it as a “bridge bank” until a buyer is found. The FDIC pays the insured depositors their deposits up to the $250,000 limit, and may also pay the uninsured depositors if the systemic risk exception is invoked.

The FDIC claims that no depositor has ever lost a penny of insured deposits since its inception in 1933. However, this does not mean that depositors are completely safe from losses. First, the $250,000 limit may not cover all of your deposits if you have multiple accounts or large balances at the same bank. Second, the FDIC may take some time to pay you back, depending on the size and complexity of the failed bank. Third, you may lose access to your money temporarily, which can cause inconvenience or hardship. Fourth, you may lose interest or dividends on your deposits, or face penalties for early withdrawal of certain accounts. Fifth, you may face tax implications or legal issues if your deposits are part of a trust, an estate, a retirement plan, or a business entity.

The costs and benefits of deposit insurance

Deposit insurance has both positive and negative effects on the banking system and the economy. On the positive side, deposit insurance promotes financial stability by preventing bank runs, which occur when depositors lose confidence in a bank and withdraw their money en masse, causing a liquidity crisis and a possible contagion effect on other banks. Deposit insurance also protects depositors from losing their hard-earned savings and encourages them to save more and invest in the economy. Deposit insurance also facilitates the resolution of failed banks by allowing the FDIC to act swiftly and efficiently without causing panic or disruption.

On the negative side, deposit insurance creates moral hazard, which is the tendency to take more risks when the consequences are borne by someone else. Deposit insurance reduces the incentives for depositors to monitor the soundness and performance of their banks, and for banks to manage their risks prudently and efficiently. Deposit insurance also distorts the allocation of resources by subsidizing risky banks and creating competitive advantages for them over safer banks or non-bank financial institutions. Deposit insurance also imposes costs on the banking industry and the taxpayers, as the FDIC charges premiums to banks to fund its Deposit Insurance Fund, and may borrow from the Treasury or impose special assessments on banks if the Fund is depleted.

The future of deposit insurance

The FDIC’s decision to invoke the systemic risk exception for Silicon Valley Bank and Signature Bank has raised questions about the future of deposit insurance and its implications for the banking system and the economy. Some argue that the FDIC should extend the full guarantee to all depositors at all banks, as this would eliminate the uncertainty and discrimination among depositors and banks, and enhance the confidence and stability of the financial system. Others argue that the FDIC should limit the guarantee to the $250,000 cap, as this would reduce the moral hazard and the costs of deposit insurance, and encourage more market discipline and diversification among depositors and banks.

The optimal design and scope of deposit insurance is a complex and controversial issue that involves trade-offs and challenges. The FDIC and other regulators should carefully evaluate the costs and benefits of deposit insurance, and balance the goals of financial stability, depositor protection, and market efficiency. The FDIC and other regulators should also monitor the risks and trends in the banking industry, and adjust the deposit insurance policies and practices accordingly. The FDIC and other regulators should also communicate clearly and transparently with the public and the stakeholders about the deposit insurance rules and expectations, and educate them about the rights and responsibilities of depositors and banks.

Related News

What is a time deposit and how does it work

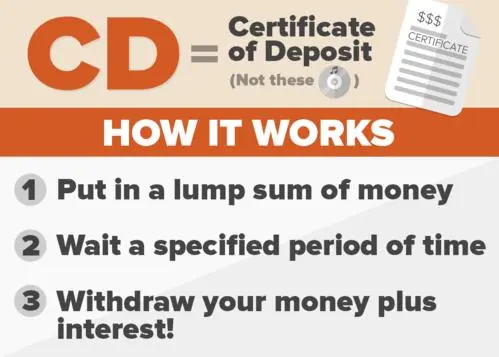

A time deposit, commonly known as a certificate of deposit (CD), is a type of savings account offered by banks and financial institutions. It operates as a fixed-term deposit where you agree to keep a specific amount of money deposited for a predetermined period, known as the term or maturity period BANKING2026-07-20

Fintech: The Key to Financial Inclusion in Nigeria

TranscriptBank of Industry is Nigeria’s oldest, largest, and most successful development finance institution. Over the last six years it has provided financing to over four million enterprises, helpin... BANKING2026-08-03

How Akwa Ibom Became an FDI Magnet by Transforming from a Civil Service State

TranscriptUdom Emmanuel took governorship of the Nigerian state Akwa Ibom in 2015. Since then he has transformed the southern coastal region from a civil service state into an attractive destination f... BANKING2026-07-15

There are several ways to deposit money in a bank

There are various ways to deposit money in a bank, and the availability of these methods can depend on the specific bank and its services. Here are some common ways to deposit money into a bank:1. Cash Deposit at the Branch:- You can visit the physical branch of the bank and BANKING2026-08-01

Advancing Financial Inclusion in Nigeria: A Journey of Transformation

Lagos, NigeriaBanking|Commercial bankingAuthor:Urum Kalu Eke, Group Managing Director, FBN HoldingsTop 5Top 5 forces that will shape international finance in 2023Top 5 female-fronted fintech firmsTop ... BANKING2026-07-18

Navigating Sanctions: European Countries Establish Trade Mechanism with Iran

Tehran, Iran. The country's oil industry has been particularly baldy hit by the recent US sanctions and this new European mechanism will not cover transactions related to this sectorFeatured|MarketsAu... BANKING2026-07-22

Udom Emmanuel’s Vision: Bringing Private Sector Discipline to Public Sector

TranscriptUdom Emmanuel took governorship of the Nigerian state Akwa Ibom in 2015. Since then he has transformed the southern coastal region from a civil service state into an attractive destination f... BANKING2026-07-11

How can I earn the highest interest on my money in the bank

Earning the highest interest on your money in a bank often involves considering different types of bank accounts and financial instruments. Here are some strategies to potentially maximize the interest you earn:1. High-Yield Savings Account:- Consider opening a high-yield savings account BANKING2026-07-05